The China Chip Conundrum: How U.S. Restrictions Accelerated the AI Power Shift They Were Meant to Stop

"Chip Gambit" questioned US export controls, "China Chip Conundrum" reveals the uncomfortable truth: Selling chips boosts China's AI; restricting them spurs their independence. No easy answers, only tradeoffs.

The US restrictions only accelerated China's push to semiconductor independence.

U.S. efforts to slow China's AI ambitions only accelerated its independence. While American chips from NVIDIA and AMD remain the world's most advanced, China is no longer a guaranteed growth market — and may never be again. Since 2022, Chinese companies have adapted at a pace few in Washington anticipated and are rapidly reducing their dependence on American-made chips.

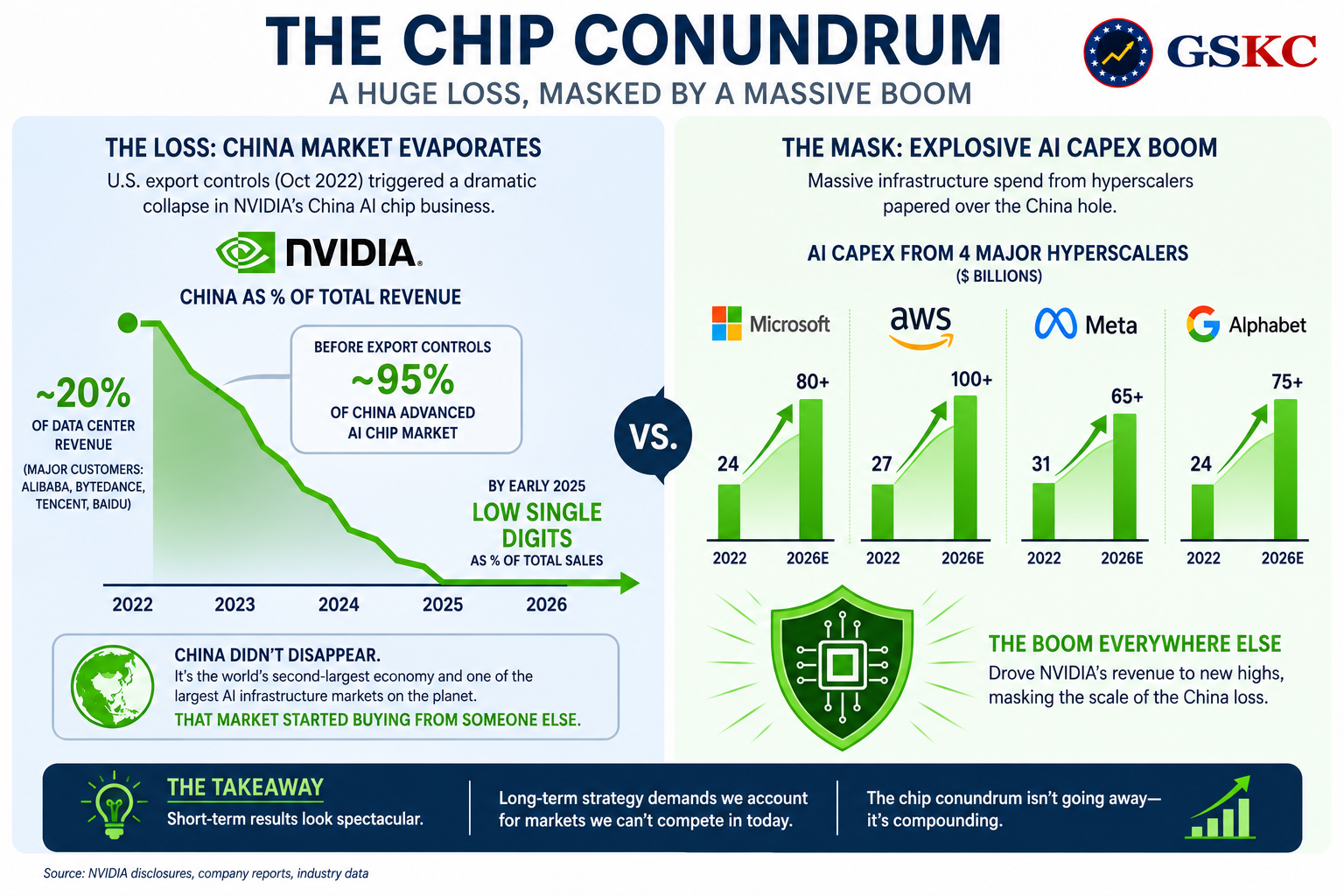

For many years, NVIDIA viewed China as one of its core growth engines. It made sense: China is home to 1.4 billion people, a surging technology sector, and the world's second-largest economy. At its peak, the country accounted for approximately 20% of NVIDIA's data center chip sales. Then geopolitics stepped in.

🔹Before U.S. restrictions, NVIDIA held nearly 95% of the advanced chip market in China

🔹China revenue collapsed from ~20% of NVIDIA's data center sales to low single digits after export controls began in late 2022

🔹Huawei's Ascend AI chips now power a growing share of domestic Chinese AI workloads.

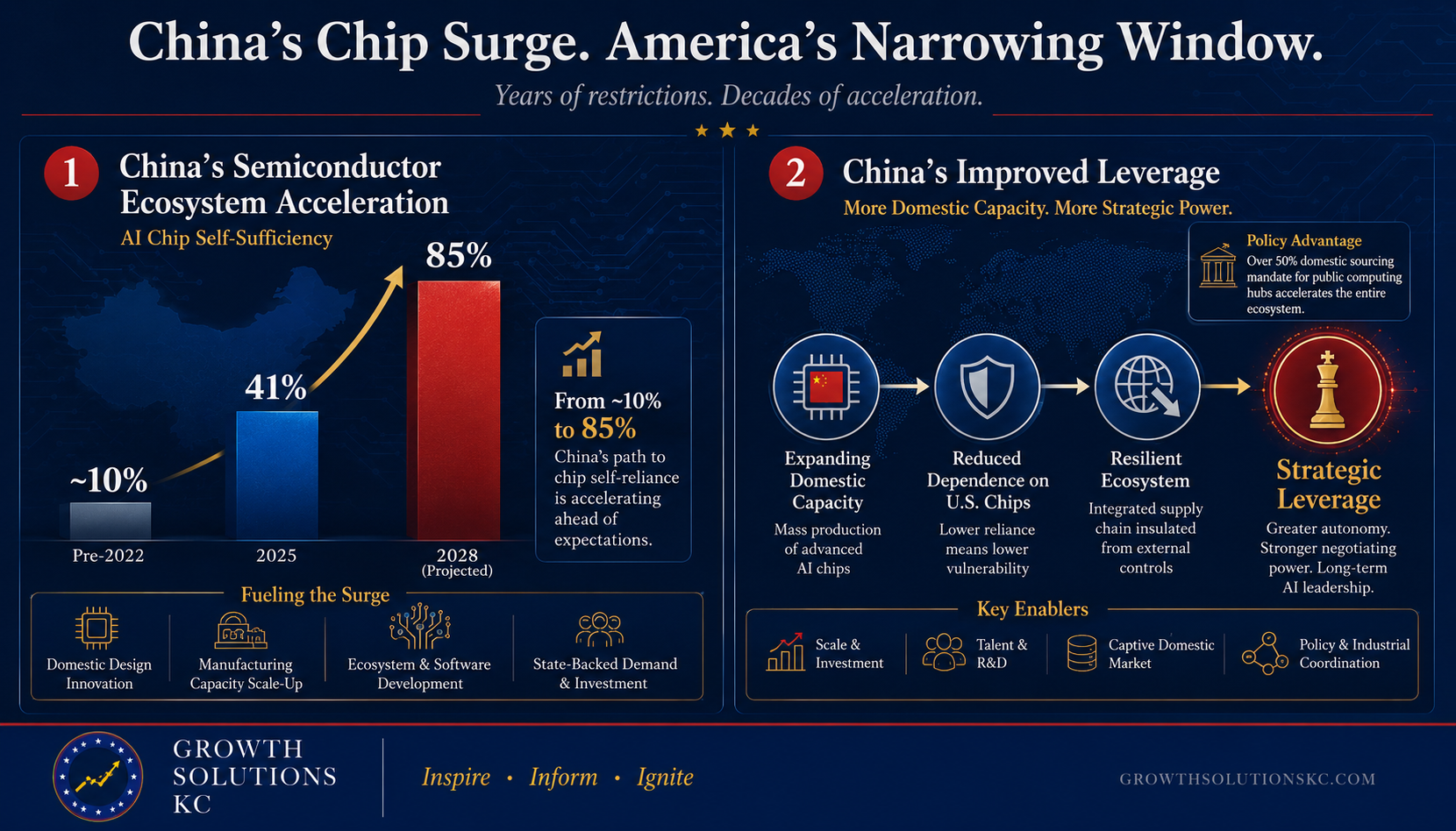

🔹China's AI chip self-sufficiency ratio has reached 41% in 2025 and is projected to hit 85% by 2028

🔹Washington's export controls left Nvidia and AMD with permanently reduced leverage in a market that may soon source up to 85% of its AI chip demand domestically.

🔹American companies lost significant revenue, global pricing leverage, and a meaningful trade negotiating card with China.

NVIDIA's China business: from boom to bust

It began with the Biden administration's export controls on advanced semiconductors and AI accelerators in October 2022. Before that, NVIDIA commanded nearly 95% of China's advanced AI chip market, with major customers including Alibaba, ByteDance, Tencent, and Baidu collectively accounting for nearly 20% of NVIDIA's data center revenue.

By early 2025, that business had largely evaporated. CEO Jensen Huang confirmed China had fallen to low single digits as a percentage of total sales — an enormous reversal for a market that once represented billions in annual demand.

What masked the scale of that loss was NVIDIA's explosive overall revenue growth, driven by massive capital expenditure from hyperscalers — Microsoft, Amazon, Meta, and Alphabet — racing to build out AI infrastructure globally. The China hole was papered over by the boom everywhere else.

But investors and strategists should not underestimate the long-term strategic cost. China remains the world's second-largest economy and one of the largest AI infrastructure markets on the planet. That market didn't disappear — it just started buying from someone else.

Is it too late for Trump's reversal?

Under the new administration, the door was partially reopened. The Trump administration approved renewed sales of NVIDIA's H200 GPUs to China, and Chinese tech companies expressed immediate interest. But the window may have narrowed permanently.

During the years restrictions were in place, China did not wait. It accelerated chip technology development, manufacturing capacity, and ecosystem construction at a pace that exceeded American expectations. China's AI chip self-sufficiency has reached 41% in 2025 and is projected to reach 85% by 2028 — a trajectory that no single product approval is likely to reverse.

Huawei is planning to produce approximately 600,000 of its Ascend 910C chips in 2026 — nearly double its 2025 output — with its full Ascend product line projected to reach up to 1.6 million dies that year. The Ascend 950 series, with self-developed high-bandwidth memory, is already on the roadmap for late 2026 onward. Beijing has also mandated that public computing hubs source more than 50% of chips domestically — creating a state-backed captive market that accelerates the entire ecosystem regardless of what American companies offer.

The aim isn't purely commercial. It's strategic. The more China depends on U.S. chips, the more vulnerable its AI sector becomes to future export restrictions. Beijing has clearly decided that vulnerability is unacceptable — and is building around it permanently.

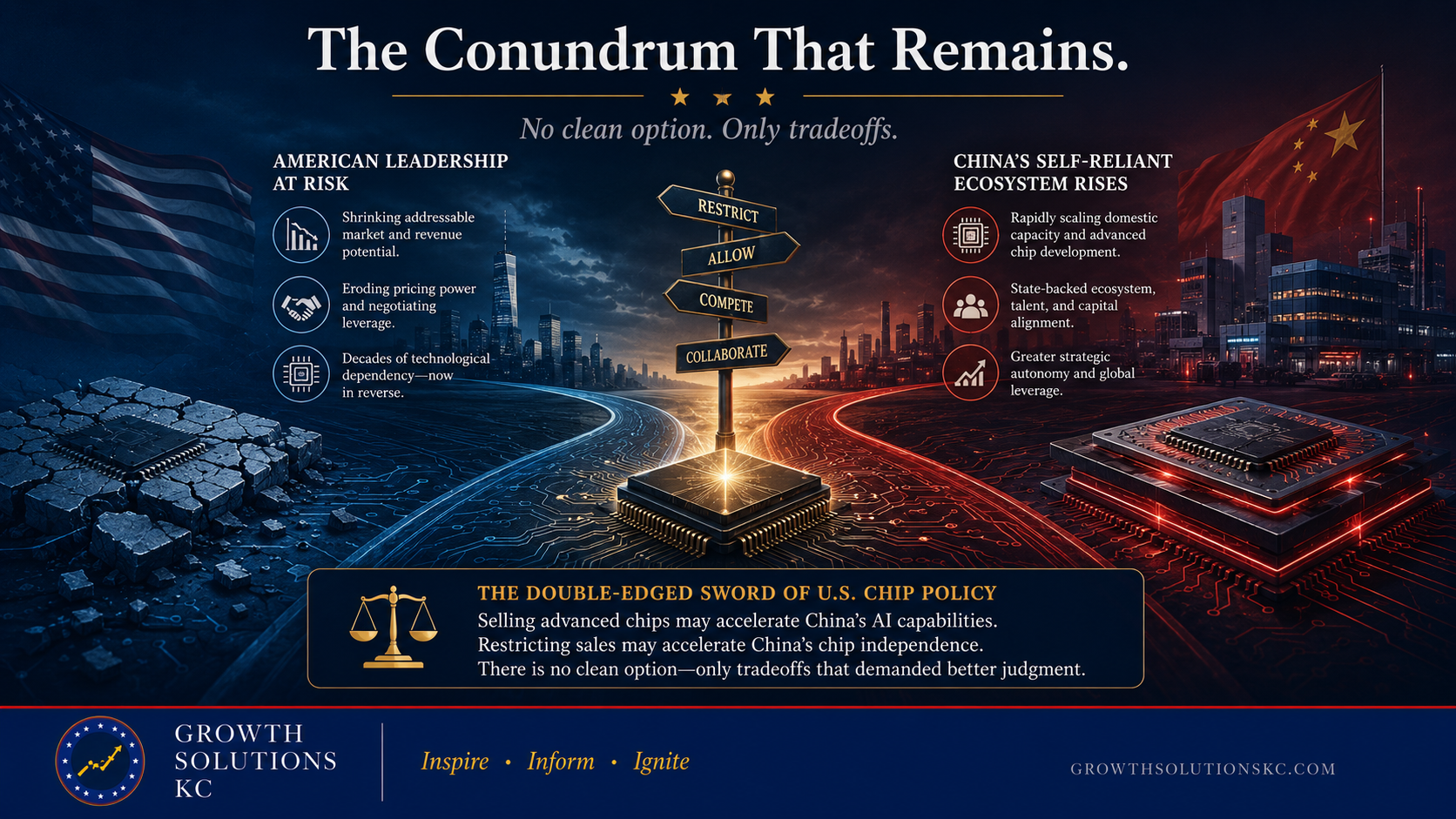

The Strategic Tradeoff Conundrum

China now has the semiconductor ecosystem in place that gives it the leverage it lacked just three years ago. When domestic manufacturers achieve supply capacity of 85% of local demand, what is lost to American companies — especially NVIDIA — is not just revenue. It is pricing power, negotiating position, and the kind of deep technological dependency that took decades to build.

This is the double-edged sword at the heart of U.S. chip policy: selling advanced American AI chips to China may accelerate their AI capabilities; restricting those sales accelerates China's chip independence. There is no clean option — only tradeoffs that needed to be weighed more carefully before the first restrictions were imposed. And there lies the conundrum.

What this means for you — the Ignite takeaway

For investors, the lesson is to assess NVIDIA and AMD not just on their current revenue strength but on the structural contraction of their addressable market. China was not just a revenue line — it was a compounding growth engine. That engine has been redirected.

For policymakers and citizens, this episode offers a durable strategic lesson: technology restrictions work best against adversaries who lack the resources, talent, or political will to adapt. Applied to a country with China's scale and national urgency, restrictions are less a wall than a starting gun. The result is a more self-sufficient, more motivated competitor — and a United States that traded long-term market leverage for short-term friction.

~ Matt Cucinotta | Growth Solutions KC | Inspire · Inform · Ignite

This is Part II in an ongoing GSKC series on the U.S.-China semiconductor conflict. Read Part I: The Chip Gambit: How America's Attempt to Slow China May Have Accelerated It.

Comments ()