Broadcom and the Burden of Dominance

When a Record Quarter Reads Like a Disappointment

Part II in the Growth Solutions KC expectation-risk series.

A Reality Check follow-up to “Nvidia and the Burden of Dominance — Understanding Expectation Risk Through the Kansas City Chiefs.”

Broadcom just gave investors a real-time case study in expectation risk.

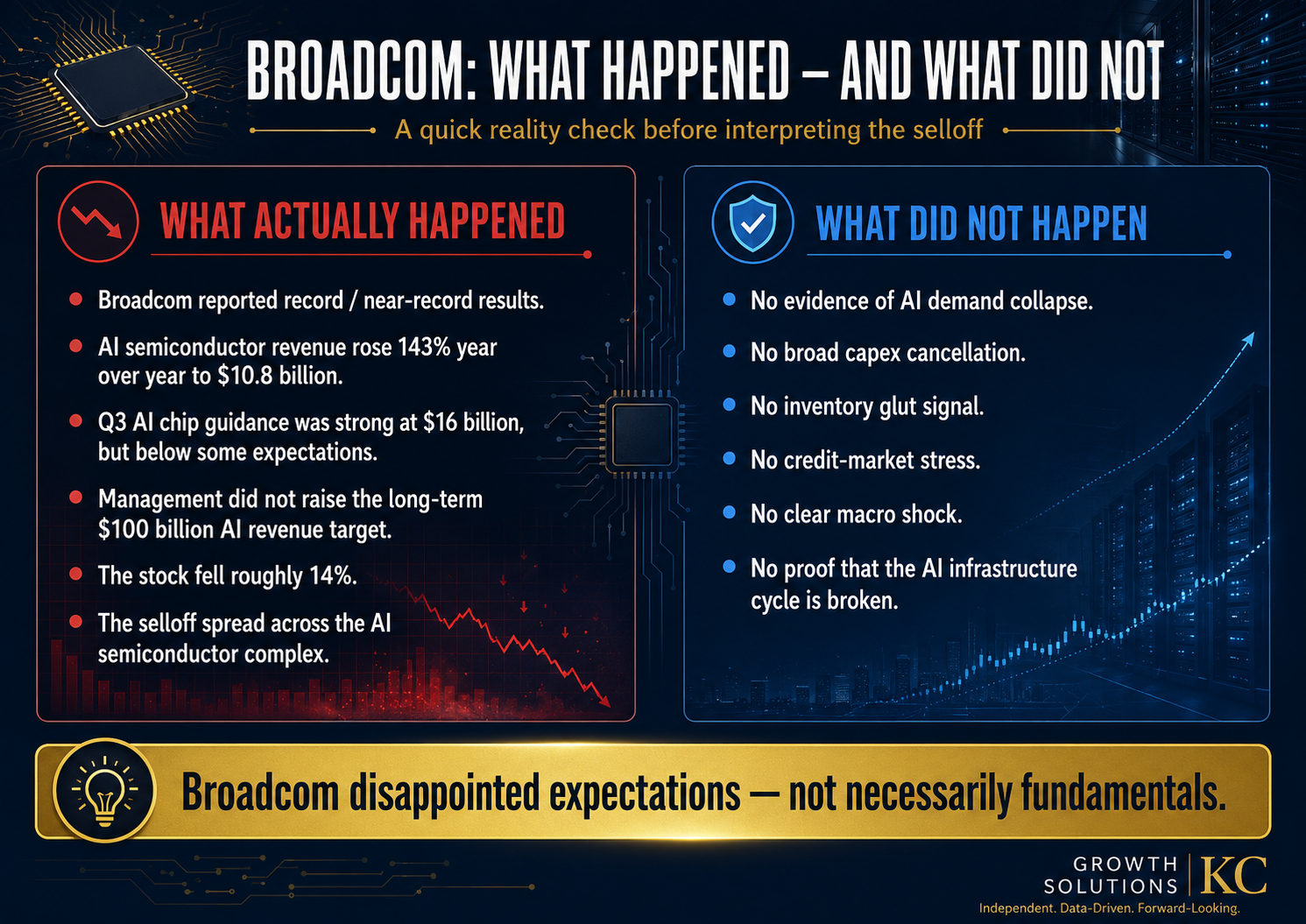

On June 3, 2026, Broadcom reported one of the strongest quarters in its history.

- Revenue reached $22.19 billion.

- AI semiconductor revenue rose 143% year over year to $10.8 billion.

- The company guided for $16 billion in AI chip revenue for the current quarter.

- Management continued pointing toward a massive long-term AI opportunity.

And the stock fell sharply.

That is the burden of dominance.

If you read our earlier piece on Nvidia, this pattern will sound familiar. We argued that the Chiefs and advanced AI chipmakers share a similar burden: once excellence becomes the norm, even outperforming expectations earns little reward, while missing an unusually high bar brings punishment.

Broadcom just demonstrated this principle in real time.

The issue was not that Broadcom suddenly became weak. The issue was that Broadcom had become expected to be extraordinary — and in a market priced for perfection, even extraordinary can read like disappointment.

In our recent Nvidia article, we argued that the market no longer rewards dominant companies simply for winning.

It rewards them for winning by more than expected.

Broadcom just demonstrated the same principle.

It is the gap between what it earned and what the market had already decided it should earn.

The Real Issue: Expectation Risk

Broadcom did not have a bad quarter. It had a strong quarter measured against unrealistic expectations.

A company can report strong revenue.

It can generate powerful AI growth.

It can guide to numbers that would have looked almost impossible a year earlier.

And the stock can still fall.

Why?

Because the market was not asking whether Broadcom was growing.

The market was asking whether Broadcom was growing fast enough to justify everything investors had already priced in.

That is a different question.

And for dominant AI infrastructure companies, it is increasingly becoming the only question that matters in the short term.

What Actually Happened

Before interpreting the reaction, it’s worth grounding in reality.

The market reaction was triggered by several factors at once.

- Broadcom’s total revenue came in slightly below expectations.

- Its AI chip revenue guidance was strong in absolute terms, but below some estimates.

- Management did not raise the long-term $100 billion AI revenue target that investors had begun treating as a baseline rather than an ambition.

- The stock had also rallied dramatically heading into the report.

In other words, investors were not positioned for good.

They were positioned for spectacular.

When Broadcom delivered strong results but did not raise the bar again, the market treated that as a disappointment.

That does not mean investors were reacting to nothing.

They were reacting to the possibility that future AI growth might not accelerate quite as quickly as the most aggressive assumptions required.

They were also reacting to legitimate questions about valuation, customer concentration, custom-chip competition, margins, and how much of the AI infrastructure boom is already reflected in share prices.

Those are real issues.

But real issues are not the same thing as a broken thesis.

What Did Not Happen

The most important part of the Broadcom selloff may be what did not happen.

- There was no evidence that AI demand collapsed.

- There was no broad cancellation of hyperscaler capital spending.

- There was no clear inventory glut signal.

- There was no pricing collapse across the semiconductor complex.

- There was no obvious credit-market stress.

- There was no proof that the AI infrastructure cycle had broken.

That distinction matters.

Markets often sell first and ask questions later. But disciplined investors must separate a stock reaction from a business reality.

A stock can decline because expectations were too high. A business declines when fundamentals deteriorate.

Those are not the same thing.

Why Semiconductors React So Violently

Expectation risk hits semiconductors harder than almost any other sector because semiconductor stocks are priced on the future.

- Not just next quarter.

- Not just next year.

- Often several years ahead.

AI semiconductor valuations depend on assumptions about data center growth, hyperscaler spending, custom silicon adoption, networking demand, power availability, memory supply, cooling needs, and the pace of artificial intelligence deployment across the economy.

That creates enormous upside when the story is working.

It also creates violent downside when the rate of change appears to slow.

Semiconductors don’t just trade on growth. They trade on acceleration.

A company growing quickly may still be punished if investors expected it to grow even faster.

- That is why a strong guide can disappoint.

- That is why not raising guidance can feel like a miss.

- That is why a single company’s report can pressure an entire ecosystem.

In most industries, meeting expectations is acceptable.

In AI semiconductors, meeting expectations can feel like falling behind.

The Shockwave Effect

Broadcom’s selloff did not stay contained to Broadcom.

That matters.

When a leading AI infrastructure company disappoints elevated expectations, investors often begin repricing the entire chain.

- Compute affects memory.

- Memory affects equipment.

- Equipment affects power and cooling.

- Power and cooling affect data center infrastructure.

The semiconductor ecosystem does not move in isolation. It moves in chains.

Broadcom’s report triggered a one-stock shockwave because investors began asking a broader question:

If one AI leader could not clear the bar, how many others are priced for the same kind of perfection?

That is why sympathy selling can spread quickly.

Some companies fall because their own thesis changed. Others fall because they sit close to the blast radius.

The discipline is knowing the difference.

Sentiment Event or Structural Shift?

The central question is simple:

Was Broadcom’s selloff a signal that the AI infrastructure cycle is breaking?

Or was it an expectation shock inside a still-intact cycle?

At this stage, the evidence points more toward the second explanation.

A structural shift would require clearer signs of business deterioration.

- Demand destruction.

- Inventory buildup.

- Pricing pressure.

- Broad capex cuts.

- Credit stress.

- Regulatory shock.

- Multiple companies cutting guidance for the same fundamental reason.

That is not what appeared here.

What appeared was a dominant company failing to exceed extreme expectations after a major run.

That is not irrelevant. But it is different.

Expectation shocks can create real volatility. They can reset valuations. They can force crowded trades to unwind. They can pressure even strong companies for weeks or months.

But unless the underlying demand cycle changes, they do not automatically become structural breaks.

What Investors Should Watch Next

The next few weeks matter.

After an expectation shock, the market usually moves through a sequence.

First comes volatility.

Mechanical selling, de-risking, momentum reversals, and exaggerated headlines often dominate the first reaction.

Then comes re-anchoring.

Analysts and long-term investors begin asking a more serious question:

Did anything actually change in the real world?

If the answer is yes, then the selloff may be identifying a deeper problem.

If the answer is no, then the selloff may be revealing a gap between expectations and fundamentals.

The key indicators to watch are not headlines. They are:

- Demand signals,

- Hyperscaler capex plans,

- AI infrastructure orders,

- Networking growth,

- Memory pricing,

- Custom-chip visibility,

- Power and cooling demand.

- Management commentary from other AI infrastructure companies,

- Credit conditions,

- and Inventory levels.

If those indicators weaken together, the story changes.

If they remain intact, the market may simply be resetting expectations after a crowded run.

The Reality Check

What Matters?

Broadcom delivered strong AI-related growth, but the market wanted more.

The company was not punished because the AI opportunity disappeared.

It was punished because expectations had become difficult to satisfy.

Why Does It Matter?

Broadcom is not just one stock.

It is part of the AI infrastructure chain.

When a company like Broadcom disappoints elevated expectations, investors begin repricing the broader semiconductor ecosystem.

That affects chipmakers, memory suppliers, equipment companies, data center infrastructure providers, and investor sentiment around the AI buildout.

What Happens Next?

Expect volatility.

Expect analysts to debate whether the selloff was overdone.

Expect investors to separate companies with intact fundamentals from companies whose expectations were simply too high.

The strongest businesses may stabilize first.

The company that triggered the shock may take longer to rebuild trust.

What Should Investors Do About It?

Do not confuse price action with proof.

Ask better questions.

- Has demand changed?

- Has the cycle changed?

- Has management changed the long-term outlook?

- Is the selling company-specific or sector-wide?

- Are related companies falling because of their own news, or because investors are de-risking the entire trade?

That is how investors separate expectation risk from fundamental risk.

Expectation risk can move a stock.

Fundamental risk can damage a company.

Long-term investors should know the difference.

The Burden of Dominance Continues

The Kansas City Chiefs are not judged like an ordinary NFL team.

Patrick Mahomes is not judged like an ordinary quarterback.

Nvidia is not judged like an ordinary semiconductor company.

And Broadcom is increasingly no longer judged like an ordinary chip supplier.

That is what dominance does.

It changes the standard.

When a company becomes one of the central players in a transformative technology cycle, investors stop asking whether it is performing well.

They ask whether it is still outperforming the dream they already priced into the stock.

Broadcom’s quarter was not weak. It was not ordinary. It was not evidence that artificial intelligence infrastructure is suddenly broken.

It was a reminder that markets do not reward excellence when excellence has already become the minimum requirement.

That was the lesson from Nvidia.

Broadcom just gave investors Part II.

A company can disappoint expectations without necessarily disappointing fundamentals.

On June 3, Broadcom did the first.

It has not yet clearly done the second.

Knowing the difference is discipline.

— Matt Cucinotta | Growth Solutions KC | Inspire · Inform · Ignite

Disclosure

This article is for educational and informational purposes only and does not constitute investment advice. Growth Solutions KC is not a licensed financial advisor. Investors should conduct their own research and consult a qualified financial professional before making investment decisions. The author may own shares or related positions in companies discussed.

Comments ()