Tax Planning Is a Year-Round Strategic Imperative

Building a practical, ongoing strategy that protects your wealth at every stage.

Looking to reduce your tax bill and keep more of your money? The answer isn't a better accountant in April. It is better decisions in January, June, and October.

Most individuals and business owners treat taxes as a once-a-year event—a seasonal hurdle to clear when the forms arrive and the deadline approaches. While that instinct is understandable, it carries a measurable, avoidable cost. By the time you sit down to file, your financial destiny for the prior twelve months is already locked in. Filing is simply a look backward; planning is where wealth is actually protected.

The structural reality of our tax code is straightforward: it rewards timing, preparation, and proactive behavior. Shifting your perspective from reactive filing to continuous strategy is where true financial control begins.

What Matters: Your Behavior Shapes Your Bill

Your tax liability is not created in the spring; it is the cumulative result of decisions made every single day. Every dollar of income received, every asset sold, every retirement contribution made or missed, and every withholding setting dictates your ultimate tax position.

The primary problem with traditional tax preparation is that it acts as a financial historian rather than a forward-facing strategist. The IRS provides high-value incentives to individuals who optimize their finances, but these doors shut firmly on December 31.

High-impact strategies cannot be deployed retroactively on April 10. They require foresight, deliberate execution, and an ongoing system.

Why It Matters: The Cost of Waiting and "Silent Tax Leaks"

When no one is actively monitoring the tax landscape during the quiet months, predictable mistakes occur. Without year-round guidance, families and small business owners frequently fall victim to avoidable financial damage:

- Withholding Errors: Families routinely under-withhold, triggering surprise penalties, or over-withhold, granting the government an interest-free loan that could have been used to build momentum elsewhere.

- Investment Missteps: Investors inadvertently trigger wash-sale rules or sell appreciated assets in the wrong tax year, needlessly inflating their bracket.

- Missed Deductions & Credits: Business expenses go undocumented contemporaneously, and distributions are taken blindly, inadvertently blowing up Affordable Care Act (ACA) premium subsidies.

Compounding this risk is the reality of a modern, highly automated IRS.

Automated matching systems — including CP2000 notices, under-reporter programs, and 1099-K expansions — mean that discrepancies in withholding or missing basis are caught instantly. These systems issue automated notices and penalties rather than opportunities to correct course. Year-round planning is the only way to close these gaps before they manifest as costly corrections.

What Happens Next: The Second-Order Effects of Proactive Planning

The immediate benefit of active tax planning is a lower bill, but the downstream effects are where real, multi-generational wealth compounds.

Furthermore, life events do not schedule themselves around filing deadlines. Major transitions carry immediate, massive, and often irreversible tax consequences:

- Getting married or divorced.

- Welcoming a child.

- Buying or selling a home or investment property.

- Starting, structuring, or exiting a business.

Navigating these shifts successfully requires a structural framework that evaluates the tax implications before the transaction closes, not after the damage is done.

What You Should Do About It: A Practical Path Forward

You do not need to become a tax code scholar to fundamentally alter your financial trajectory. Implementing a few consistent habits will transition you from a reactive posture to a strategic one.

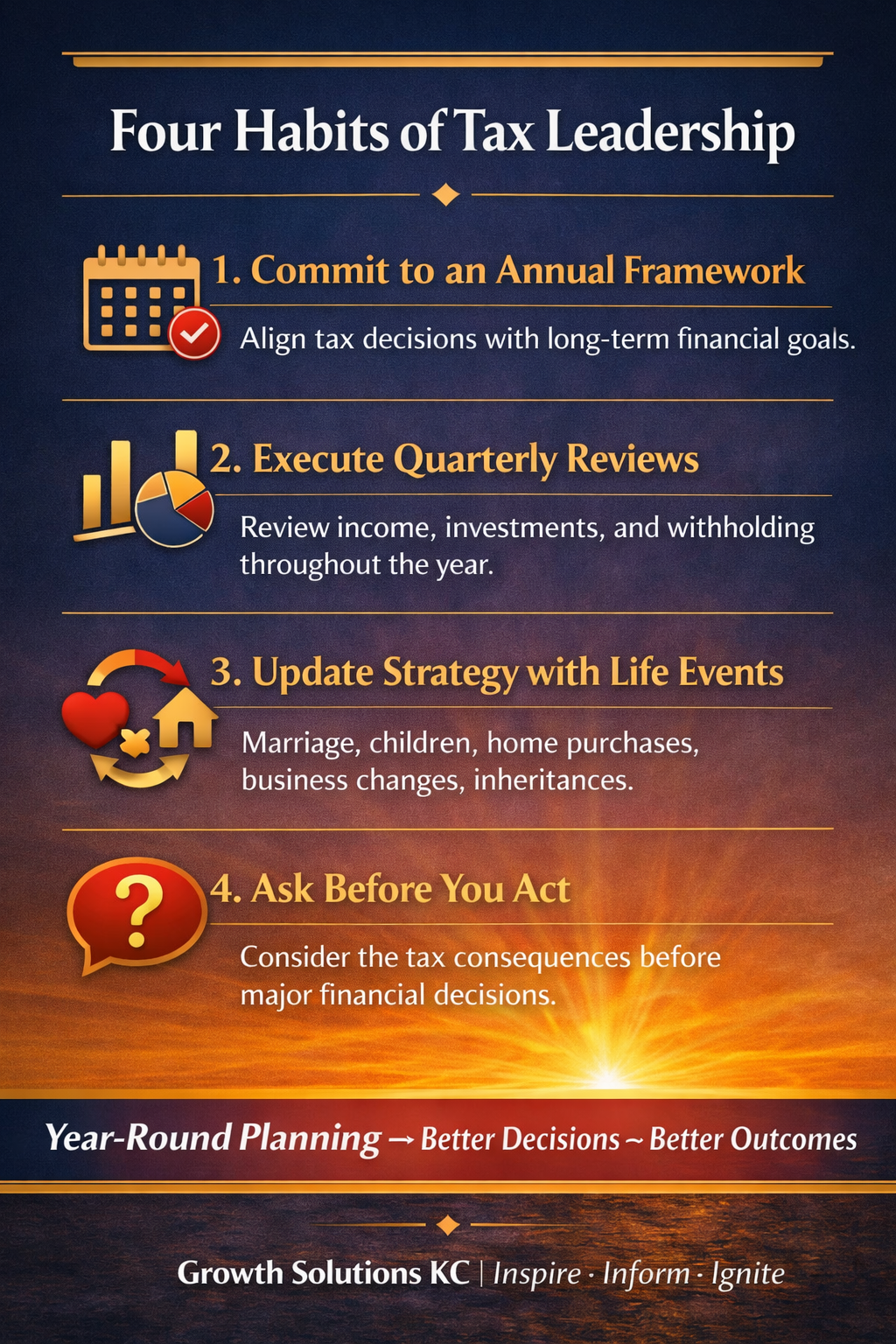

1. Commit to an Annual Year-Round Framework

Stop viewing tax strategy as a brief panic in March. Establish a year-round baseline that aligns your financial decisions with your long-term goals.

2. Execute Quarterly Strategic Reviews

Do not wait for year-end to assess your position. Every quarter, take a high-level view of your income, investment moves, and business expenses. A mid-year checkup in June or July is particularly critical to catch under-withholding or update safe harbor estimated payments while you still have months left to pivot.

3. Update Your Strategy Real-Time with Life Events

The moment a major life change occurs—whether it is an inheritance, a change in corporate compensation, or a business expansion—immediately adjust your tax projection.

4. Ask Before You Act

This single discipline prevents more financial leakage than almost any other. Before taking a large retirement distribution, shifting health plans, or liquidating a position, explicitly ask: "What are the second-order tax consequences of this move?"

The Bottom Line

Tax planning is not about finding obscure loopholes or gaming the system. It is about understanding reality, analyzing incentives, and making deliberate decisions that respect the rules of the code. In an environment that explicitly rewards timing, failing to plan is a choice—one that carries a distinct, measurable penalty. Treat strategy as a year-round discipline, and gain the clarity, predictability, and confidence that true financial leadership demands.

— Matt Cucinotta | Growth Solutions KC | Inspire · Inform · Ignite

Comments ()